Thursday, 15 January, 2026г.

Где искать: по сайтам Запорожской области, статьи, видео ролики

пример: покупка автомобиля в Запорожье

Seasonal Effects and other Anomalies

У вашего броузера проблема в совместимости с HTML5

У вашего броузера проблема в совместимости с HTML5

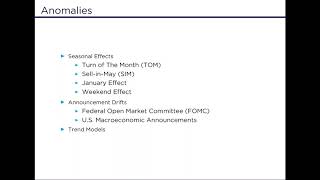

In this webinar, we will revisit a series of popular anomalies: seasonal, announcement, and momentum. We will comment on statistical significance and the persistence of these effects, proposing useful investment strategies to incorporate this information. We will also investigate the creation of a seasonal trend model composed of the Sell in May (SIM), Turn of the Month (TOM), Federal Open Market Committee pre-announcement drift (FOMC), and the State Dependent Momentum (SDM). Using the total return S&P 500 dataset starting in 1975, we will estimate the parameters of each model on a yearly basis, based on an expanding window and then proceed to form, in a walk forward manner, an optimized combination of the 4 models using the return to risk optimization procedure.

Petra Bakosova is the Chief Operating Officer at Hull Tactical. Her background is in algorithmic trading across multiple asset classes, mathematical modeling, and risk management. She joined Hull Investments, LLC in 2014, and worked on projects for its proprietary trading firm Ketchum Trading, LLC before transferring to its quantitative asset management unit HTAA, LLC. Ms. Bakosova has helped shape the face and direction of HTAA prior to and since the launch of its first public product and continues to perform research on a number of HTAA strategies. Ms. Bakosova began her career in quantitative finance at Arbhouse, LLC as the company’s first strategist. Her expertise in high frequency algorithmic market making proved to be a valuable precursor to the systematic, quantitative approach sought after at HTAA. Prior to Hull Investments, she cut her teeth on stock market indices modelling during her tenure as a quantitative researcher at Toji Trading Group, LLC. Ms. Bakosova holds a Master of Science degree in Financial Mathematics from the University of Chicago. She pursued her undergraduate studies in applied mathematics at the Comenius University in Bratislava, Slovakia and Halmstad University in Halmstad, Sweden.

To learn more about Quantopian, visit http://www.quantopian.com.

Disclaimer

Quantopian provides this presentation to help people write trading algorithms - it is not intended to provide investment advice.

More specifically, the material is provided for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation or endorsement for any security or strategy, nor does it constitute an offer to provide investment advisory or other services by Quantopian.

In addition, the content neither constitutes investment advice nor offers any opinion with respect to the suitability of any security or any specific investment. Quantopian makes no guarantees as to accuracy or completeness of the views expressed in the website. The views are subject to change, and may have become unreliable for various reasons, including changes in market conditions or economic circumstances.

Теги:

finance quantitative finance risk risk analysis math statistics algorithms algorithmic trading

Похожие видео

Мой аккаунт