Tuesday, 13 January, 2026г.

Где искать: по сайтам Запорожской области, статьи, видео ролики

пример: покупка автомобиля в Запорожье

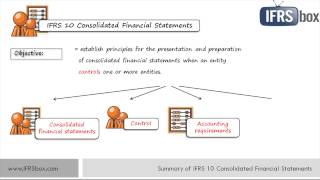

IFRS 10 Consolidated Financial Statements - summary

У вашего броузера проблема в совместимости с HTML5

У вашего броузера проблема в совместимости с HTML5

http://www.ifrsbox.com This is the short summary of IFRS 10 Consolidated Financial Statements. The objective of IFRS 10 is to establish principles for the presentation and preparation of consolidated financial statements when an entity controls one or more other entities. IFRS 10: - requires to present consolidated financial statements; - defines the principle of control - sets out the accounting requirements for consolidated financial statements and - defines an investment entity and sets out an exception to consolidating particular subsidiaries of an investment entity. An investor controls an investee when It is exposed to or has rights to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee. Consolidated financial statements are the financial statements of a group presented as those of a single economic entity. Consolidation procedures: Step 1 – Combine like items of assets, liabilities, equity, income, expenses and cash flows of the parent with those of its subsidiaries. Step 2 - Offset or eliminate carrying amount of parent’s investment in subsidiary with parent’s portion of equity of each subsidiary. Step 3 - Offset or eliminate in full intragroup assets, liabilities, equity, income, expenses and cash flows relating to transactions between companies in the group. Investment entity is an entity that: - Obtains funds or money from one or more investors for the purpose of providing those investor(s) with investment management services; - Its business purpose is to invest funds solely for returns from capital appreciation, investment income, or both; and - It measures and evaluates the performance of substantially all of its investments on a fair value basis. If you’d like to learn how to consolidate, or anything about IFRS in general, please visit http://www.ifrsbox.com and subscribe to our free IFRS mini-course. Thank you!

Теги:

IFRS 10 IFRS consolidation How to consolidate IFRS lectures IFRS videos IFRS training IFRS courses IFRS group accounts Consolidated Financial Statement International Financial Reporting Standards

Похожие видео

Мой аккаунт